You can stop living paycheck to paycheck

Not with a budget - with a cash plan

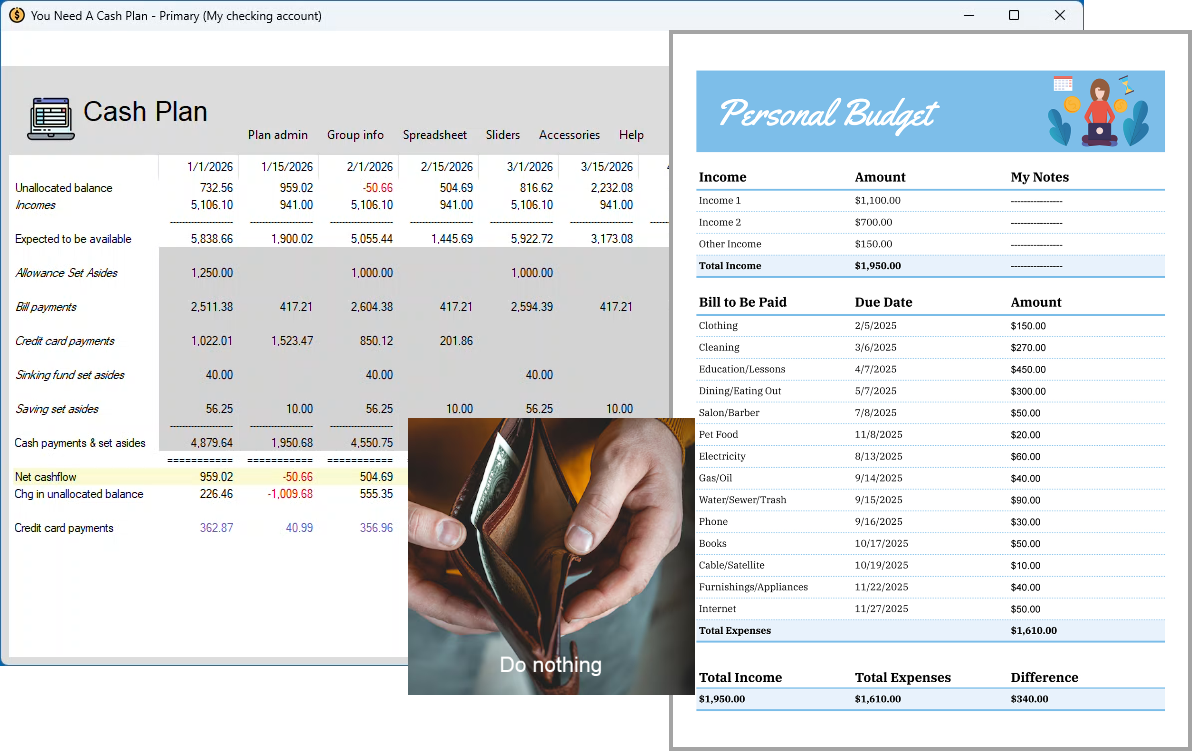

Build your cash plan

mbr-buttons mbr-theme-style="display-4" class="mbr-section-btn mt-3" mbr-if="showButtons" data-toolbar="-mbrBtnMove"Read the book free